24 August 2023

Steven Slaughter, Lead Portfolio Manager

CJ Sylvester, Portfolio Manager

COVID-19 is largely behind us in terms of a global health crisis and a hard hit to global financial markets. Yet, amid a widely predicted economic recession, the world is adjusting to the post-pandemic era. In this Q&A, Steven Slaughter, Lead Portfolio Manager, and CJ Sylvester, Portfolio Manager, highlight how our Global Healthcare Team adopts a differentiated approach by triangulating its investment thesis and quantifying key inputs into the investment framework.

As the Macroeconomic Strategy Team highlighted in its Global Macro Outlook Q3 2023, the recession has been postponed, not cancelled. Market concerns about a U.S. economic recession will likely be carried over to the second half of this year.

As our investors know, the healthcare sector remains one of the most recession-resistant areas of the economy. It has been a defensive stalwart during enhanced volatility and economic uncertainty. In particular, the outperformance of healthcare in recent economic downturns was primarily due to inelastic demand for medical resources.

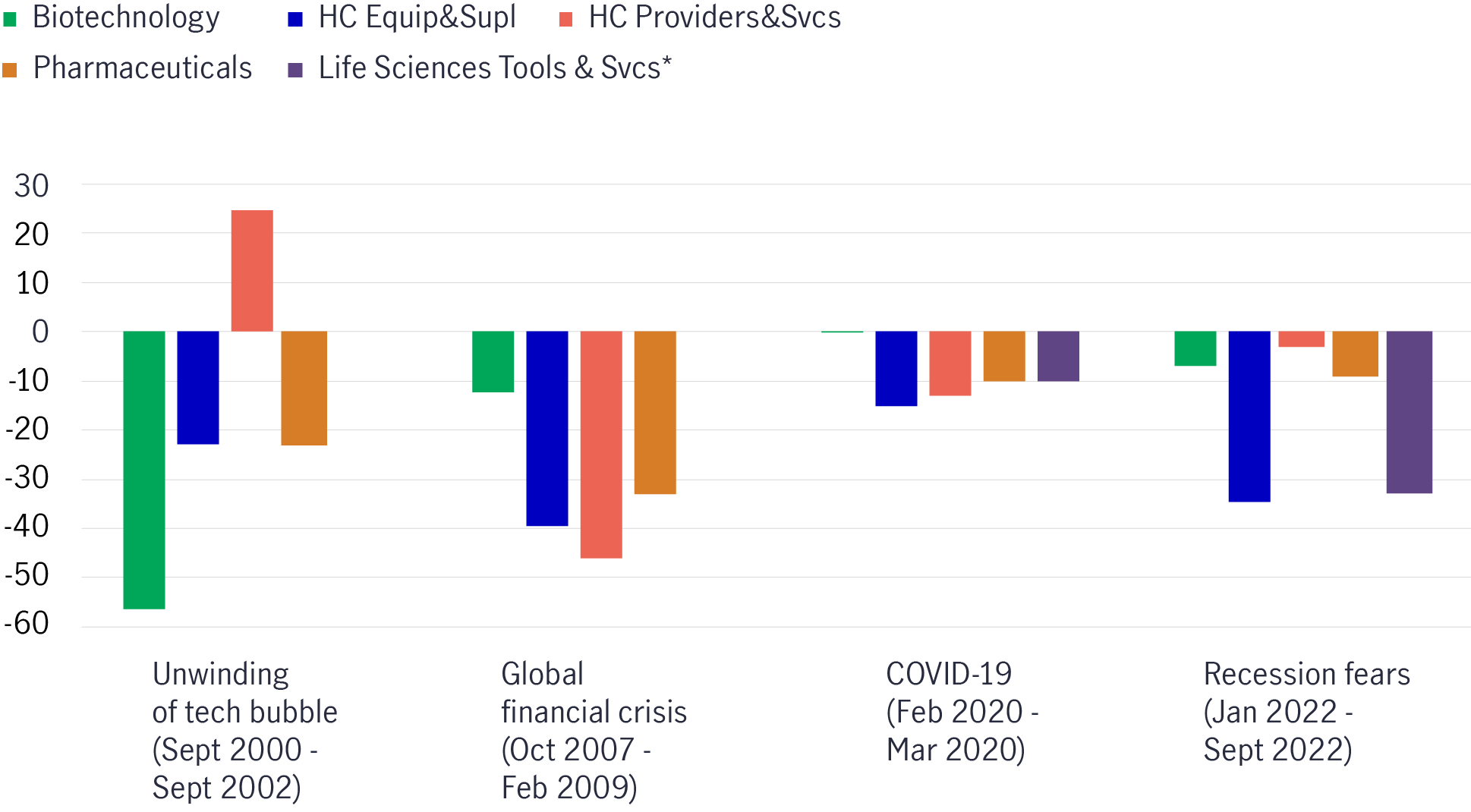

During the most recent recessionary periods, sub-sector dispersion was wide. Pharmaceuticals generally provided good, sometimes better, protection, while biotech outperformed in three out of the recent four market downturns. Also, healthcare providers & services witnessed increased returns in the last three recessions. (Refer to Chart 1).

Chart 1 Healthcare equities showed resilience during recent economic downturns

Source: FactSet, all other industry returns from Morningstar, Inc. Past performance is not indicative of future results. It is not possible to invest directly in an index. Y-axis represents the index returns. Biotechnology refers to MSCI World/Biotechnology GR (USD), HC Equip&Supl refers to MSCI World/Health Care Equipment & Supplies GR (USD), HC Providers&Svcs refers to MSCI World/Health Care Providers & Services GR (USD), Pharmaceuticals refers to MSCI World/Pharmaceuticals GR (USD) and Life Sciences Tools & Svcs refers to MSCI World/Life Sciences Tools & Services GR (USD). *Returns during the unwinding of tech-bubble and global financial crisis are not available.

The proprietary fundamental research conducted on a daily basis by seasoned investment professionals with solid medical backgrounds underpins our differentiated investment approach. On average, our portfolio managers have over 30 years of experience spanning large-scale multinational healthcare corporations to global asset management firms. This has laid a solid foundation that helps us make vital investment considerations across the broader healthcare landscape. Slaughter’s educational background in biology, as well as Sylvester’s in biology, neurobiology, and physiology, empower our team with the knowledge base to effectively engage with the medical and scientific communities on the cutting-edge technologies and advancements within healthcare. This, combined with deep industry expertise required for dedicated fundamental research enable us to uncover compelling investment ideas before they are fully appreciated by a broader cohort of market participants.

Besides traditional fundamental equity analysis via investment screens and financial modelling, our team devotes energy and passion to building an in-depth and insightful scientific understanding of the healthcare sector. This is based on proprietary fundamental research from:

During the research process, our team members act as stewards, proactively attending company meetings and investor conferences, liaising with industry thought leaders, as well as engaging with C-suites and board members (not limited to only companies owned in our portfolio). Our long-standing corporate relationships also enable the team to conduct objective environmental, social, and governance (ESG) analysis of risks and opportunities – driving the positive change that could benefit long-term, value-driven company growth.

The longevity of our on-the-ground research capabilities is instrumental in the bottom-up decision-making process. This includes: i) evaluating end-market size and product demand, ii) identifying product-pipeline strength and conducting competitor product analysis, and iii) assessing the strength of management teams.

Given our passion for the ever-changing healthcare industry, we monitor and digest medical journals and scientific publications from a practitioner’s viewpoint. This approach ensures we are aware of medical advances in pharmaceutical and therapeutic landscapes. As a result, we can avoid over-reliance on secondary or sell-side research, allowing us to independently evaluate markets, uncover hidden ideas, develop in-depth analysis, and make judgements beyond financial numbers and market sentiment. The art of marrying quantitative and qualitative inputs is our main proprietary asset for idea generation – a unique interactive research process that could unlock underappreciated market opportunities.

As we highlighted in our 2023 outlook, Manulife IM’s fundamental research process has identified a series of published research studies noting increased morbidity among patients recovering from COVID-19 infections and, as evidenced by, an elevated risk of cardiovascular diseases, diabetes, and central nervous system (CNS) diseases relative to the uninfected population. Coupled with the unmet medical needs for pre-existing conditions, we believe that opportunities abound for experienced investors with keen insights who can identify underappreciated market opportunities and deliver outperformance. Our approach continues to inform how we evaluate investment opportunities across the healthcare universe. To this end, the findings mentioned above relating to structural changes in healthcare (including, but not limited to, long COVID) support the urgency to manage other pre-existing diseases effectively, diagnoses that our research suggests pre-dispose these comorbid patients to higher morbidity and mortality from COVID-19. For example, we continue to look at companies with novel treatments for CNS diseases (depression, Alzheimer’s) and continue to focus on orphan diseases (i.e., those affecting fewer than 200,000 individuals). We see a greater understanding of the genetic causes of these diseases, and those learnings are being applied to novel drugs that could dramatically impact patients. We are also identifying smaller biotech names with significant upside and alpha generation potential, given that these companies’ innovations are in the final phases of clinical development.

Overall, we believe the healthcare sector will remain one of the most defensive segments in any potential economic recession scenario. Additionally, the unprecedented innovation and medical advancements expected in a post-COVID-19 era should provide a fertile opportunity set for market beating growth. Our differentiated research approach, underpinned by experienced and seasoned investment professionals with solid medical backgrounds, allows us to look beyond financial figures and market sentiment to identify companies with potential upside and alpha generation at an earlier stage than others.

We continue to see unprecedented demand among companies with products and services that address all three guiding principles: i) unmet medical needs, ii) underappreciated market opportunities, and iii) the ability to bend the healthcare cost curve.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

China Fixed Income: From deflation to reflation: what comes next?

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global Equity Diversified Income (GEDI) strategy update: Risks and opportunities

In early April, developments in the Middle East showed signs of stabilisation, prompting a partial recovery and renewed risk-taking in equity markets. However, beyond ongoing geopolitical risks, other factors—including potential private credit contagion across banks and broader financials—continue to pose downside risks. Despite these uncertainties, we believe an income centric approach, combined with global diversification across growth, value and income equities, has provided both downside resilience and upside participation for the Global Equities Diversified Income (GEDI) strategy.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))